"The company's management's judgment on Gome's future solvency has changed significantly." On April 25 this year, whirlpool issued an announcement publicly questioning the cash flow capacity of Gome retail. According to whirlpool, from 2021 and 2022, the company sold 79.58 million yuan and 8.81 million yuan to Gome respectively, and the accumulated accounts receivable of 87.1 million yuan was delayed.

Author Guo Haiwei

Since then, Gome's retail share price has continued to fall and kept hitting new lows. So far this year, it has fallen nearly 40% and the price per share is less than HK $0.5.

In February last year, when Huang Guangyu issued an open letter to "return to the original market position in 18 months", the company's share price was still HK $2.55.

For Whirlpool's suspension of cooperation and the questioning of Gome's cash flow ability, Gome has issued a long response statement. Gome said, "there is no delay in the payment of goods, and it still owes about 10 million yuan for various expenses and 20 million yuan for unsalable and defective products."

In addition, Gome also directly stated in the article that "whirlpool has chaotic management, simple and rough handling, and lack of integrity", "product quality is not strictly controlled, problems occur frequently, and consumers complain repeatedly [enter the black cat complaint]", and the announcement behavior "is actually to solve the Galanz problem".

Although the facts stated by both parties are large, the rationality of Gome's data is questionable. The main reason is that the amount of appeal in Gome's report is too large.

If the arrears of 10 million yuan and defective products of 20 million yuan are true:

Then Whirlpool's additional marketing investment in Gome channels will account for 11% of the total sales revenue. According to Whirlpool's financial report, the gross profit margin of whirlpool home appliance manufacturing is only 8.7%, and the overall net profit margin is negative.

And according to Gome & amp; According to Whirlpool's policy of quality assurance and renewal within 15 days, the proportion of defective products of whirlpool products in Gome channel will also be about 20% during the dispute period.

Obviously, neither of them is a regular number for a brand like whirlpool.

Source: whirlpool official website

The conflict between Gome and well-known brand manufacturers seems to be more and more frequent.

On April 19, several media reported that an official letter from Midea Group was circulated on the Internet. The official letter said that on April 15, "the employees of Jinan Gome branch 'physically assaulted the employees of Gome". Because Gome has not replied to the specific solution for a long time, Midea China decided to withdraw all products from GOME Jinan.

Gome subsequently said that the incident was "a serious operation and management accident" and would be "dealt with seriously" and "notified of warning". Gome hopes to "turn bad things into good things and promote the further deepening of bilateral cooperation".

A former employee of Gome expressed regret for pinplay:

"In the past, Gome was disobedient and dismissed you from GOME stores. Now it can't. We have to beg others not to quit."

For brands, channel means the revenue and profit of real gold and silver. Now, whether Midea or whirlpool, the brand side often says that Gome, as a channel side, will exit, and the decline of Gome's control in the channel may be just one of them.

Gome may need to reflect more on whether the brand relationship maintenance strategy is appropriate and whether it can still achieve the desired effect by maintaining its habitual "wolf" style.

Source: dressing up home

Whirlpool is not the only one questioning Gome's liquidity.

According to pinplay, Gome's internal employees are increasingly worried about the group's cash flow problems, and layoffs, salary cuts, underperformance and other phenomena continue to occur in various departments.

A recently resigned employee of Gome told PinWan that the headquarters of Gome has successively laid off staff since this year. The proportion of layoffs in various departments of the headquarters is different, ranging from 20% to 40%. Recently, there are rumors that it will face more large-scale layoffs.

Whether the employees who stay or have left, they are faced with the situation of delayed performance. Some Gome employees said to pinplay, "only half of the performance and year-end awards have been issued."

At the same time, many Gome employees said that the company was planning "contract replacement" for large-scale employees. Its main content is to transfer some monthly performance and monthly basic salary into annual performance. Many employees believe that the annual performance is not stable, and there is a suspicion of a 20% pay cut in a disguised form when signing a contract. If an employee does not sign a new contract, he will be threatened by HR to leave.

Pinplay consulted a number of Gome related persons and said that the operation of changing and signing the contract was basically true.

Pulse source: pulse source

From public information, Gome's cash flow level is indeed at a recent low value.

Taking Gome's financial report data as an example, in 2021, Gome's cash and general equivalents were only 4.378 billion, a decrease of more than 50% compared with 9.597 billion in 2020, the lowest value in many years. In contrast, Gome's current liabilities remained at an all-time high of 52.149 billion, only a slight decrease of 1.5% from 52.9 billion in 2020.

In other words, Gome's current cash scale is only 8.3% of current liabilities.

On the other hand, Gome's operating cash flow remained low in 2021, and the annual net operating cash flow was only 630 million. The annual operating profit loss was as high as 4.072 billion, and the net profit loss was as high as 4.72 billion. Although the loss has narrowed significantly compared with the loss of RMB 6.9 billion in 2020, it is still high as a whole.

The difference between operating cash flow and net profit is also the core reason for the deterioration of the relationship between Gome and brands. When the channel providers cannot make profits through the market as a whole and the business scale is not further enlarged, it means that the difference between loss and net profit actually comes from the zero sum game of the accounting period.

Under this background, the relationship between the two sides may collapse.

This year, if Gome fails to turn its overall business around in time, it will be more difficult for Gome to maintain a net increase in its operating cash flow. Once there is a run on suppliers like whirlpool and Gome's cash reserves are insufficient, Gome will naturally be very passive.

Therefore, on the whole, Gome's current cash flow situation has been in a very tight state.

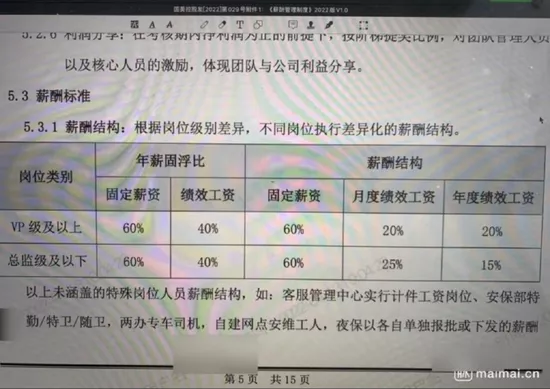

According to the financial report, Gome's accounts payable period and the turnover days of notes payable are 175 days in 2020, which is the figure reached when it is reduced from 187 days in 2021. In contrast, JD's accounting period is about 7-9 weeks, and that of its old rival Suning is 60 days. Some brands and suppliers in the latter two have been complaining secretly.

These 175 days are just the average of Gome's accounting period. Generally speaking, the payment terms of big brands in the channel will be relatively good; Small and medium-sized brands with worse voice will have worse cashing conditions. Taking whirlpool as an example, as a market waist brand, according to its announcement, the brand should have not paid for 16 months.

Even if calculated according to the 175 day accounting period, it has meant huge financial pressure for brand suppliers, which actually exceeds the affordability of most small and medium-sized sellers in the market.

A relevant person from GOME told pinplay that Gome had hoped to promote may day and other festivals, hoping to alleviate the overall business pressure through the promotion.

According to the above financial figures, Gome will occupy more accounts payable and increase the short-term pressure on cash flow if it puts too much pressure on treasure at this time. The final result will naturally make the relationship between short-term channels, brands and employees more severe.

Source: Network

From the perspective of public information, the current tight cash flow of Gome retail mainly comes from the long-term failure to improve the operating conditions and the changes in the market environment.

On the one hand, Gome has been facing the problem of scale decline in the past few years.

From 2018 to 2021, Gome's revenue fell from 65.289 billion to 46.925 billion, while the number of inventory turnover days remained almost unchanged, which meant that the annual flow fell by 18.3 billion.

Gome's fiscal period in 2018 is 148 days. If calculated according to the fiscal period of 175 days in 2021, it means that there is about 4 billion yuan of available cash loss - equivalent to the current cash reserves.

On the other hand, Gome faces sustained losses of real gold and silver.

In the four years from 2018 to 2021, Gome's retail accumulated a loss of 18.8 billion yuan, which once pushed Gome to the brink of insolvency.

In 2020, Gome's net assets will be only 1.26 billion yuan; In 2021, through a series of capital and share increases, the net assets rebounded to 17.5 billion - but it actually included a new 20-year use right of 17.8 billion to the leased site of Gome holdings, which soared its "use right assets" to 24.88 billion yuan.

Considering the current market value of less than 10 billion yuan, Gome's lease is more than twice as expensive as Gome.

Photo source: how happy

Compared with the already optimistic financial situation, the more difficult problem for Gome is that it seems to have been unable to find a better source of incremental cash flow.

The shortening of the accounts payable cycle from 181 days to 175 days means that Gome's strategy of unlimited pressure on the account period has actually been unsustainable - in fact, the ultra long account period of 181 days has shown that Gome's procurement and marketing team has "done enough" and demonstrated the excellent negotiation ability of Gome's supply chain team. However, such an accounting period is fundamentally unsustainable and undermines bilateral trust.

Both the real happy mall and offline store chain hoped by Gome, or its own 3C sales field, are facing the dilemma of weak growth.

According to the data of several reports, in Q1, the total amount of China's home appliance market decreased by 11% year-on-year, and the shipment volume of mobile phone market decreased by 14%. The above two categories account for more than 90% of Gome's revenue (2020 data), which undoubtedly further increases the difficulty of Gome's operation this year.

A number of Gome related people said that Gome's cash flow pressure is indeed higher than last year.

Source: Netease viewer

In addition, Gome still seems to have serious data misleading behavior in the key data of key businesses.

Pinplay exclusively reported the news that Xiang Hailong, President of Gome online, and Zhang Deju, CEO of electric appliance company, left one after another in June last year. At that time, the article pointed out the problems existing in Gome's internal corporate culture, employment ethics, office integrity, brand relationship and industry structure, and questioned the authenticity of the true happiness data and the formulation of "returning to the market position in 18 months".

But a year later, while Gome did not release its revenue data, it was still unilaterally increasing its really happy monthly living figure.

According to Gome, in 2021, the annual traffic of zhenhappy was 440 million, and the annual active buyers reached 16.837 million.

However, according to Fang Wei, CFO of Gome and other news, zhenhappy's monthly life exceeded 40 million in the first quarter, 50 million in June and 65 million in December. If this growth curve is calculated - if this is really a continuous curve, the monthly activity of each person alone is more than 440 million.

Based on 0 person / month from January to February, 40 million person / month from March to may, 50 million person / month from June to November and 65 million person / month from December, the total number of "monthly living people" should be 485 million - about 110% of the "annual visits".

In the face of all-round pressure, it is time for Gome to take seriously the monthly activity and transaction data disclosure of online platforms. Frankly facing the current business difficulties and gaining the trust and respect of more partners and employees is the best way to get out of the dilemma as soon as possible.