There were two large-scale "delisting tides". More than 170 Chinese concept companies bid farewell to Wall Street. The "return of Chinese concept shares" has also become a hot word in the capital market. What are the reasons behind the delisting of these companies? Where should they realize their value in the future? Is the US stock market no longer attractive? The reporter of the international finance news and the experts conducted in-depth exploration on these issues

In 1992, brilliance motor, the "first share of China concept", was listed on the New York Stock Exchange, which has been 30 years since.

Over the past 30 years, more than 500 Chinese companies have listed in the United States, and "China concept stocks" have once become the most active focus in the U.S. capital market.

However, influenced by changes in the overseas regulatory environment, the gradual improvement of China's domestic capital market system, and China US relations, a large number of China concept companies have withdrawn from the US market in the past decade.

In 2022, in the face of intensified regulatory frictions between China and the United States and the continuous evaporation of market value, where should China concept stocks go?

Two delisting waves

According to incomplete statistics by the reporter of the international finance news, as of May 20 this year, China concept shares have experienced two waves of large-scale delisting, and more than 170 China concept shares enterprises have delisted.

Since 2010, the short selling institutions represented by muddy water and citron have started a series of hunting against the financial fraud of zhonggai shares, and Oriental paper, Rino technology, China high-speed channel, etc. have been sniped. In 2011 alone, more than 45 China concept stock companies were shorted, and the "China concept stock trust crisis" broke out.

Later, US investors' concern about vie structure risk led short sellers to launch a second round of sniping at New Oriental, Huishan dairy, focus media, Anta sports and other companies. As a result, many zhonggai shares have suffered serious losses and their market value has shrunk. Shanda network, focus media, Peking University qianfang and other companies have chosen privatization to withdraw from the U.S. market. The privatization return of focus media has brought the temptation of high valuation, which has set off the first wave of China concept shares' active privatization and delisting.

On january31,2020, muddy water released the short selling report of Ruixing coffee. Ruixing's financial fraud attracted the attention of the U.S. regulators, which once again plunged into a crisis of confidence in the U.S. and China concept stocks. Iqiyi, tal, who to learn from and other enterprises also suffered from short selling. In addition, the US regulators' increasingly strict audit and information disclosure of China concept shares, and the second wave of China concept shares delisting started.

Recently, "with the intensification of the game between China and the United States, the United States has continuously strengthened the regulatory policy involving China concept shares, expanded the list of securities trading restrictions, introduced and accelerated the implementation of the foreign company Accountability Act, and increased the restrictions and information disclosure requirements for enterprises with variable interest entity structure. The regulatory environment of China concept shares market has undergone profound changes, and the uncertainty has increased significantly, resulting in the delisting pressure of most China concept shares." Zhaoxueqing, a researcher at the Bank of China Research Institute, said in an interview with the international finance news.

According to liruomu, a partner of Meifu law firm, China's series of regulations on overseas listing and securities issuance of Chinese companies, as well as the regulations on the exit of sensitive data and information, have made some Chinese concept shares seriously consider whether they can meet the requirements of laws and regulations of China and the United States at the same time, and whether the cost of maintaining listing and compliance in the United States is too large. In addition, although the U.S. stock index has been at a high level recently, the valuation of zhonggai shares has been continuously reduced, which also makes some investors interested in privatization take the initiative to contact zhonggai shares whose current valuation is lower than their actual value, especially companies with good operation, high-quality management and no regulatory risk in the industry will be favored by investors. At the same time, the domestic listing system is gradually in line with international standards. For example, companies with red chip structure established in Cayman are allowed to be listed on the science and innovation board, which provides a way for companies after privatization to be listed again.

These are the reasons for delisting

Kuangyuqing, founder of lens research, summarized the main characteristics of stock concept during delisting in the past decade in an interview with the international finance news: first, loss of sustainable operation ability, second, forced delisting due to fraud, and third, privatization and active delisting due to low valuation.

The reporter of the international finance news selected 158 delisted Chinese stocks (excluding SPAC) from 2012 to 2022 as samples, and found that 35 (22%) of them were delisted, 79 (50%) of them chose privatization, and 17 (10%) of them announced active delisting.

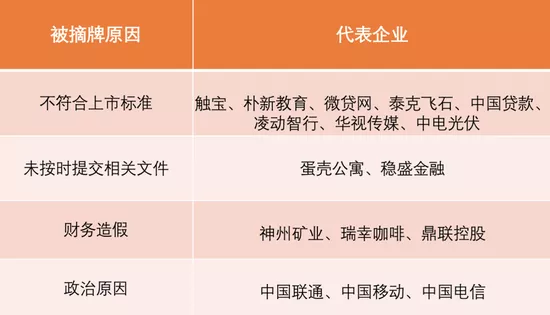

Most of the delisted enterprises fail to meet the listing standard of maintaining an average market value of at least US $15million within 30 consecutive trading days, or the closing price is less than US $1 per share for the last 30 consecutive working days; Some enterprises failed to submit relevant documents required by SEC on time or were found to have made financial fraud; And partly for political reasons.

In the opinion of investment bankers, there are four main reasons for some zhonggai stocks that choose to delist or privatize voluntarily:

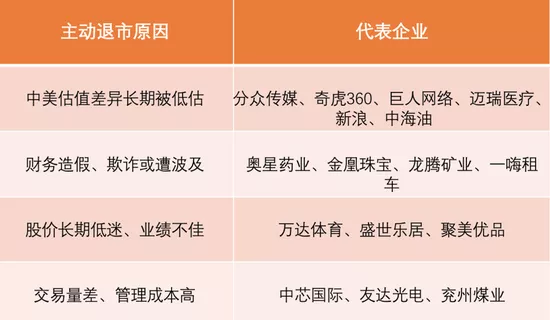

First, the difference in valuation between China and the United States makes some Chinese concept stocks undervalued. The high P / E ratio, overvalued value and high financing amount in the domestic IPO market have always been attractive to these companies;

Second, part of the financial fraud of China concept shares has spread to companies with good quality, and delisting under regulatory pressure has become a natural choice;

Third, the stock price has been depressed for a long time and the performance has been poor;

Fourth, after listing in the US market, the transaction volume is poor and the maintenance cost is high.

China US game promotes backflow

Over the past decade, China and the United States have played a game around the audit draft, and Ruixing's financial fraud reached a climax in 2020.

In march2021, the US Securities and Exchange Commission passed the final amendment to the foreign company Accountability Act, which requires that foreign issuers who fail to meet the inspection requirements of the US public company accounting oversight board (PCAOB) on accounting firms for three consecutive years shall be prohibited from trading their securities in the US.

Since the beginning of March this year, the SEC has published the list of 7 batches of "pre delisted" Chinese stocks. So far, there have been 139 zhonggai shares included in the list. A total of 23 companies in the first four batches have passed the time limit for pleading and are included in the "confirmed delisting list", and the fifth batch is about to enter the "confirmed delisting list", which includes station B, Zhongtong, JD, pinduoduo, Tencent music, Ctrip, etc.

As for the audit negotiation on China concept shares, the latest news shows that the SEC believes that there are still some problems in the audit negotiation between China and the United States on China concept shares. The CSRC said that the audit and inspection problems should be solved through cooperation on the basis of equality, and the CSRC's attitude has always been positive and constructive.

Fangxinghai, vice chairman of the CSRC, stated at the Boao Forum on April 21 that the negotiation between China and the United States on auditing was smooth. He believed that a cooperation agreement could be reached soon and was confident that the relevant uncertainties would be eliminated soon.

In an interview with the media, Li qiusuo, managing director and chief strategic analyst of CICC research department, said that as the Chinese and US regulatory authorities are moving in the opposite direction and exploring the possibility of achieving sustainable regulatory cooperation, this has dispelled the market's concern about the extreme delisting of Chinese stocks to a certain extent.

Kuang Yuqing is also optimistic about the final compromise agreement reached between China and the United States on cross-border supervision, and believes that there will be no collective delisting of China concept shares.

However, he also believes that if the main business of the company is closely related to national defense, military industry, national security and information security, it is estimated that it is difficult to avoid delisting from US stocks.

"According to the regulations, China concept stock companies should submit the audit draft before the end of 2023, otherwise they will be forced to withdraw from the market. Some China concept stock companies, especially financial, military, large technology companies and other enterprises involved in sensitive industries of the country, have to withdraw from the U.S. market." Zhaoxueqing told the international finance news.

Wang Jun, director of China's chief economist forum, told the international finance news that from the current situation, the vast majority of China concept shares may be delisted from the United States. This is not a technical problem that can be solved by strengthening cooperation and coordination between regulatory authorities, but is determined by the overall background of competition and confrontation between China and the United States in the fields of finance, science and technology, intellectual property rights and so on.

However, according to Li Feng, an accounting professor at Shanghai Advanced Institute of finance, the delisting of China concept shares from the United States is not entirely inevitable. Whether these companies must delist in twoorthree years depends to a greater extent on the final communication results between the regulatory agencies of the two countries. However, because the capital market most repels uncertainty, in this process, zhonggai shares will bear great market pressure.

Back to a or back to Hong Kong?

If delisting is inevitable, what kind of outlet should we look for in the U.S. - China equity companies?

Over the years, overseas listing has become one of the important financing channels for Chinese enterprises. In a broad sense, China concept shares generally include listed companies in Hong Kong. In the case of excluding Hong Kong shares, the United States and Singapore are the two most preferred markets for China concept shares from the point of view of listing location, and a small number of China concept shares are listed in Canada, the United Kingdom, Australia and other places.

Under the delisting risk, the return of zhonggai shares has become a hot word in the capital market. All parties in the market are actively preparing for the return of China concept shares to Hong Kong shares or a shares. But whether to return to a or Hong Kong is a question worth pondering.

In the two delisting waves in recent years, in order to raise funds to maintain business, some Chinese companies seeking to be listed in the domestic capital market, such as returning to the A-share market, listing on the new third board, or going to Hong Kong for secondary listing, etc.

Liruomu said that some companies have been dual listed in Hong Kong or Singapore in order to avoid risks, but privatization is the direction of consideration for some zhonggai companies with low market capitalization and can not fully meet the criteria for dual listing.

Focus Media delisted on NASDAQ in 2013. In 2015, it returned to A-share by backdoor 7xi holdings, with a market value of more than 260billion yuan, ten times that when it exited from US stocks. As the first case of the return of zhonggai shares to a shares, focus media created a textbook template of "privatization delisting + backdoor listing" for latecomers.

In july2016, qihoo360 was officially delisted from the New York Stock Exchange with a market value of US $9.3 billion, becoming the largest privatization transaction among Chinese companies listed in the United States at that time. "The $8billion market value does not fully reflect 360's corporate value." Zhou Hongyi, founder, chairman and CEO of 360, explained the reasons for delisting. In 2018, 360 returned to a shares, and then its market value increased 7 times.

In 2021, after the NYSE launched the delisting procedures for China Mobile, Chinatelecom and China Unicom, the three major Chinese telecom operators withdrew from the US market, and then "joined forces" in a shares one after another. However, in the past ten years, the three major telecom operators have completed the task of listing in the Hong Kong stock market after issuing ADR in the US stock market.

The openness, vitality and competitiveness of mainland China's capital market are further increasing. The plan of comprehensive registration system was announced at the beginning of this year. Under this system, the A-share market will further move towards market orientation and focus on the quality of information disclosure.

Wang Jun also pointed out that the mainland stock market has been committed to building a multi-level capital market and promoting the reform of relevant basic systems in recent years, and has made some positive progress, such as the establishment of the Beijing stock exchange and the reform of the registration system for stock issuance. However, considering historical and practical factors, the listing rules and standards, trading systems and costs, financing systems and costs, regulatory rules, product categories, valuation characteristics Obviously, there are great differences in many aspects, such as securities culture, degree of internationalization, breadth and depth of investors. These will be important factors that enterprises need to consider when selecting the listing location.

Zhangzhenzhen, chief analyst of the communications industry of Anxin securities, said that the high listing threshold, large differences with the U.S. stock listing system and legal system, and high exit costs of investors all affected the re listing of China concept shares to a shares. However, the A-share trading volume is larger and the liquidity is stronger. It is expected that the return of China concept shares will obtain a more ideal valuation. Subsequent policy support may attract companies with good performance to land.

"Safe haven"

In contrast, it seems that the feasibility of China concept stock returning to Hong Kong stock market is higher.

Hong Kong's capital market has always been positioned as the preferred destination for overseas listing of mainland Chinese enterprises. Most insiders believe that the Hong Kong capital market is the main "safe haven" for China concept shares.

According to the report of CICC in May this year, at present, 27 China concept shares have returned to Hong Kong shares in different forms, including 5 privatized delisted companies, including China flying crane, Wuxi apptec, E-House China, Sansheng pharmaceutical and Le Dou game, and 6 dual listed companies (Baiji Shenzhou, ideal automobile, etc.). Since the reform of Hong Kong's listing system in 2018 paved the way for the secondary listing of China concept shares in Hong Kong, 16 China concept shares have been listed in Hong Kong.

The agency predicts that 42 companies may meet the conditions for secondary listing and return to Hong Kong stocks in the next three to five years, and it does not rule out that overseas issuers will also seek "safety cushion" under unexpected risks by means of Dual Major listing.

The Hong Kong market of China is also actively adjusting the listing system of overseas issuers. Since 2018, the Hong Kong market has begun to create favorable conditions for the return of China concept shares, including the revision of the main board listing rules by the Hong Kong Stock Exchange in 2018, allowing China concept shares to be listed in Hong Kong for a second time; In october2019, the company will accept the secondary listing of the same shares with different rights.

However, not all China concept shares meet the conditions for returning to Hong Kong.

According to the CICC report, about 200 U.S. zhonggai shares are temporarily unable to meet the threshold for the secondary listing of Hong Kong shares, but their market value accounts for only about 15% of the total scale of the part that has not returned. "Although it is difficult to meet the return conditions for the time being, there is no need to be too pessimistic. For at least three years, we believe that zhonggai shares, which are temporarily difficult to meet the return time and market value requirements, still have enough time to prepare for listing.".

At the time of the full return of China concept shares, the market is worried about whether the Hong Kong stock market can bear the valuation and liquidity of China concept shares.

Linmingtian, chief analyst of atfx Asia Pacific region, told the international finance news that since 2019, Alibaba, Netease, jd.com, New Oriental, autohome, Baidu, Ctrip, B station and Weibo have returned one after another, which once caused the market value of Hong Kong stock Hang Seng Index to expand and the index reached a peak. However, times have changed, and the strong performance of Chinese stocks delisted in the United States may not come again in the future.

"Compared with the volume of the US stock market, there is actually no room for substantial improvement in the revaluation of the China concept stocks that have returned to Hong Kong," Lin said.

At present, the global stock market is dragged down by factors such as the tightening of monetary policies by major central banks and the conflict between Russia and Ukraine. The external market was originally in poor mood. Hong Kong stocks have fallen nearly 20% since their high in January this year. The overall decline of Chinese stocks in Hong Kong is also large, and some individual stocks have fallen more than 50%.

Hong Kong's "competitors" are also eager to try.

Singapore is gradually becoming another place for the return of China concept shares after Hong Kong. On May 20, Wei Lai, one of the new forces in car making, introduced the listing method in the Singapore Stock Exchange. Weilai became the first Chinese enterprise listed in New York, Hong Kong and Singapore at the same time. In response to media questions, a spokesman for the Singapore Stock Exchange said that he hoped to provide options for China concept shares.

In addition to open market financing, the financing channels of enterprises are becoming diversified.

Wang Jun said that enterprises can also choose private equity, debt financing and endogenous financing. "In fact, for the vast majority of enterprises serving the mainland market, the current domestic multi-level market system should be able to meet the diversified financing needs and transaction exit arrangements of enterprises in terms of breadth, depth and future development prospects. Except for individual industries and fields, the superiority of the Hong Kong market over the mainland market may be gradually reduced in the future.".

Sudden drop in attractiveness of listing in the United States

The channels for Chinese enterprises to list overseas are still open, but the ringing of Wall Street is no longer attractive.

On May 17, Chinese Vice Premier Liu he stressed the need to properly handle the relationship between the government and the market, and reiterated his support for relevant enterprises to list abroad.

Yi Huiman, chairman of the CSRC, also said that the CSRC will accelerate the implementation of new regulations on the supervision of overseas issuance and listing of enterprises, maintain smooth channels for overseas listing, and support Chinese enterprises to make better use of two markets and two resources in accordance with the law.

Although the United States still provides a competitive capital market, it is no longer the best choice for Chinese enterprises.

"This year, one China concept stock has been listed in February, and several other companies have submitted listing applications to the sec." Liruomu said, "The SEC also issued detailed disclosure guidance on vie structure risks, specifying how to disclose the risks involved in vie structure operation and the risks related to government policies and regulations; the company needs to clearly explain the necessity of obtaining approval from CSRC, State Grid Information Office and other relevant departments, and whether its auditors meet the review requirements of PCAOB. The SEC's clear guidance has made it possible for some Chinese companies to predict their future listing in the United States . Meanwhile, some Chinese companies are also in the process of listing in the United States through spac. Of course, before China and the United States reach an agreement on the differences over reviewing the audit draft, more companies are still waiting and watching. "

Zhaoxueqing believes that the mature and developed U.S. venture capital system is crucial for high growth enterprises. In addition, listing in the United States also has positive value for optimizing the equity structure of enterprises and expanding overseas business. However, with the intensification of the game between China and the United States, the financial channels in the United States have been blocked, and the attractiveness of listing in the United States has decreased significantly.

Kuang Yuqing said that listing in the United States will no longer be the main goal of most Chinese companies, unless it has been determined in the bet agreement that it is necessary to list in the United States. "The probability of taking the initiative to list in the United States is low. In the past two years, the share price has plummeted, and the valuation has been unable to reasonably show its value. In this case, continuing to promote the listing in the United States is not to maximize shareholders' interests, but to maximize losses.".

"Recently, although Wall Street is generally bullish on China concept stocks, in the long run, going to the United States for listing is of little significance, because the confidence of both sides is not the market itself, but political factors. It is unpredictable what measures the United States will take to suppress China concept stocks in the future. If it goes to the United States for listing due to short-term factors at this time, it will leave many complex and difficult market problems." Kuang Yuqing said.

"It is basically impossible for Chinese enterprises to go to the United States for listing in batches as the tide in the past. There will certainly be some individual cases, which will also become a sign of the relaxation and phased improvement of bilateral relations." Wang Jun said.

Reporter Yuanyuan, lixizi