The revenue of the world's top five chip design giants is experiencing a fault. Qualcomm, Broadcom, MediaTek and NVIDIA have entered the top five chip design companies for ten consecutive years, while amd has ranked top 5 seven times in the past decade. Last year, AMD's revenue was $11.6 billion more than the sixth place.

▲ from 2018 to 2021, the ranking of the world's top ten chip design companies was calculated by revenue (data sources: trendforce, IC insights, note: trendforce ranking Qualcomm only calculated the revenue of QCT department, NVIDIA deducted OEM / IP revenue, Broadcom only calculated the revenue of semiconductor department, which was different from the company's financial report data)

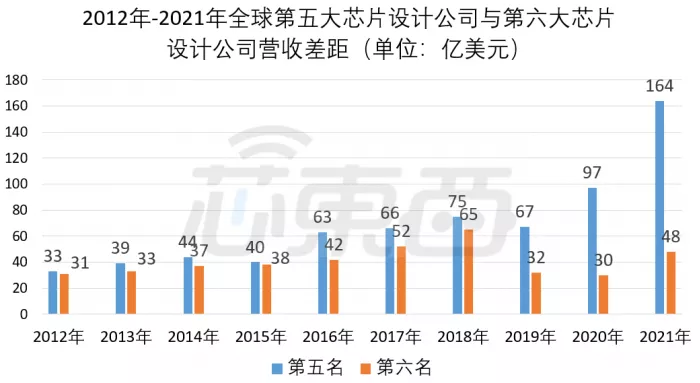

In 2021, the revenue of the top five chip design companies was between us $33.6 billion and US $16.4 billion, and the revenue of the last five in the top 10 was between us $4.8 billion and US $1.5 billion. AMD, which ranks fifth, needs the combined revenue of chip design enterprises from sixth to ninth to compete.

In the past ten years, the change from the sixth to the tenth place has not only been greater, but also the revenue gap between the top five plants and the bottom five plants in the top 10 has become larger and larger in recent three years. In 2019, the fifth AMD's revenue was more than double that of the sixth Xilinx, with a difference of US $3.5 billion; AMD, which still ranked fifth in 2021, has more than twice the revenue of the sixth Lianyong technology, with a gap of US $11.6 billion.

In 2021 alone, the total revenue of the top ten chip design companies reached US $127.405 billion, of which the top five accounted for more than 85%.

More importantly, in the past two years, dialog, which originally ranked tenth, was annexed by Japanese semiconductor giant Renesas, and Xilinx, which ranked ninth, will be acquired by AMD. As giant acquisitions continue to change the semiconductor pattern, this fault is gradually increasing.

In February this year, amd has completed the acquisition of Xilinx, the ninth largest chip design company and FPGA leader. The revenue of the two sides will be merged in 2022. At that time, the revenue of one AMD company is likely to be higher than the sum of the last five chip design companies in the top 10.

01. Over the past decade, the world's top 10 chip design giants have changed

According to IC insights, in 2012, the top ten chip design companies in the world were Qualcomm, Broadcom, AMD, NVIDIA, MediaTek, Marvell, LSI, Xilinx (acquired by AMD in 2022), Altera (acquired by Intel in 2015) and Avago.

At that time, the revenue of the fifth MediaTek and the sixth Meiman Electronics was US $3.3 billion and US $3.1 billion respectively, with a difference of only US $200 million. In 2021, the revenue gap between the fifth place AMD and the sixth place Lianyong technology has opened to US $11.6 billion. The sum of the annual revenue of the sixth place Lianyong technology + the seventh place Meiman electronics + the eighth place Ruiyu + the ninth place Xilinx is only US $16.5 billion, US $100 million more than AMD.

▲ revenue gap between the fifth largest chip design company and the sixth largest chip design company in 2012-2021

In February this year, as the regulatory authorities of various countries have approved AMD's acquisition of Xilinx, amd has announced the completion of the acquisition, and its revenue will soar again. The revenue of AMD + Xilinx has been higher than the sum of the last four chip design companies.

Over the past decade, new chip design companies have been appearing on the list. Huawei Hisilicon, Spreadtrum (later acquired by Ziguang group and merged with radico to form Ziguang zhanrui), Lianyong technology and dialog are all typical enterprises.

However, most of these emerging enterprises rank low. The four giants of Qualcomm, Broadcom, MediaTek and NVIDIA have never fallen out of the top five and established their leading advantages early. Amd has been hovering between the third and sixth places, and has continuously entered the top 5 since 2019.

Among the five chip giants, Qualcomm is the leader in smart phone SOC and RF front-end, and also has a large number of communication patents. In 2021, Qualcomm's revenue reached US $33.566 billion. The main revenue growth included smart phone products, RF products and Internet of things products, and ranked as the world's largest chip design company.

NVIDIA is the absolute leader in the global GPU market, with a revenue of US $26.91 billion in fiscal year 2022. It is the second largest chip design company in the world.

Broadcom is an old semiconductor giant in the United States. It has a high market share in various semiconductor products and corresponding software services, such as set-top box SOC, wired network chip, RF front-end, Wi Fi chip and so on. In 2021, Broadcom's revenue reached US $27.45 billion, ranking third.

MediaTek is a major competitor of Qualcomm and has layout in smart phone SOC, TWS headset chip, Internet of things chip and other fields. In 2021, MediaTek's revenue was NT $493.415 billion (about RMB 1127.95), making it the largest manufacturer of smartphone SOC shipments.

However, although today's top five chip design companies were already the leaders of the industry as early as a decade ago, the revenue gap between the fifth and sixth place only appeared in recent three years.

02. Backed by key markets, semiconductor M & A intensifies and faults appear

From 2019, the revenue gap between the top five chip design giants and the bottom five manufacturers in the top 10 began to gradually widen. This is not only because the top five chip design giants have gained advantages in the market earlier, but also because they are in the fast-growing markets such as smart phones, data centers, 5g and PCs.

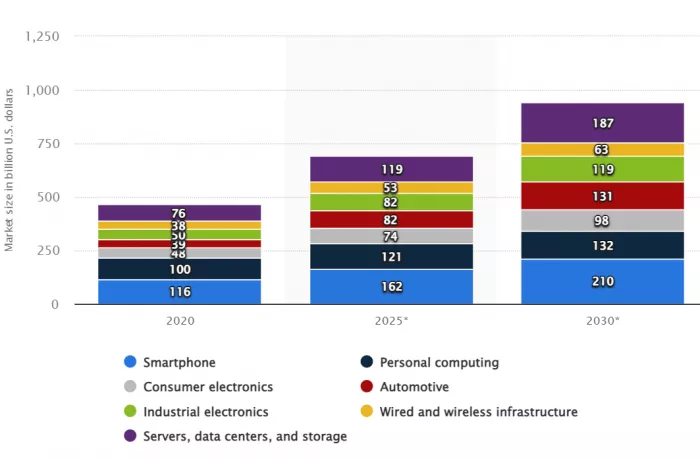

According to statistics firm statista, from 2020 to 2030, smart phones are the largest segment of the global semiconductor market. The smart phone semiconductor market will reach US $116 billion in 2020, and this figure may become US $210 billion by 2030.

Behind smartphones are PCs, servers, data centers and storage. In 2020, the sales of the two types of semiconductors were US $100 billion and US $76 billion respectively, which happens to be the business scope of the five chip design companies of Qualcomm, NVIDIA, Broadcom, MediaTek and AMD.

▲ global semiconductor sales by market (source: statista)

From 2018 to 2021, three of the top 10 chip design companies fell behind, but these companies fell out of the list not because of market competition or the rapid growth of revenue of other chip design manufacturers. The fact is that Huawei Hisilicon, dialog and Xilinx no longer appear on the list due to factors such as being sanctioned by the United States or being acquired by other industry leaders.

In 2018, Huawei was included in the list of entities by the U.S. government. Huawei Hisilicon, which has the ability to design 14nm smartphone SOC, is difficult to obtain the capacity of wafer factories such as TSMC. Kirin 9000 has become the masterpiece of Huawei 5g mobile phone SOC. After that, Huawei mobile phones can only use 4G SOC.

In 2020 and 2021, Xilinx, one of the top ten chip design companies in the United States, and dialog, an old analog chip factory in the United Kingdom, were successively launched for acquisition. Now both acquisitions have been completed.

In October 2020, amd launched the acquisition of Xilinx, with an acquisition amount of US $35 billion. In February 2022, the State Administration of supervision conditionally approved AMD's acquisition of Xilinx. After that, amd announced the formal completion of the acquisition of Xilinx.

▲ amd announces completion of acquisition of Xilinx

In February 2021, Japanese auto chip giant Renesas Electronics announced its acquisition of dialog for us $6 billion. In August 2021, Renesas Electronics announced the completion of the acquisition of dialog. From October 1 of the same year, Vivek bHan, former senior vice president and general manager of dialog, took over as senior vice president and deputy general manager of automotive solutions business department of Renesas electronics.

In 2021, dialog will no longer be among the top ten chip design companies in the world, but will be replaced by Qijing optoelectronics, a display driver chip design company in Taiwan, China. In 2022, after the merger of AMD and Xilinx, its revenue scale may be further improved, which will open the gap between the world's top five chip design companies and the sixth to tenth places again, and the fault of the top five chip design giants will increase again.

03. Top five chip design giants create Legends

In addition to market and M & A factors, the top five chip design giants also stand out from the heavy competition and have their own legends.

1. Qualcomm: started from communication, defeated Deyi and became the king of mobile SOC

Among the top five manufacturers, Qualcomm was the first wireless communication technology company established in 1985. In 1989 and 1993, Qualcomm introduced division multiplexing (TDMA) and division multiplexing (CDMA) respectively, creating communication standards in the 2G and 3G era.

In 2000, Qualcomm sold its mobile phone and network equipment business, focusing on the research and development of communication technology and mobile SOC. Due to its accumulation in the communication field and patent wall, Qualcomm surpassed Texas Instruments to become the world's largest wireless chip supplier in 2007.

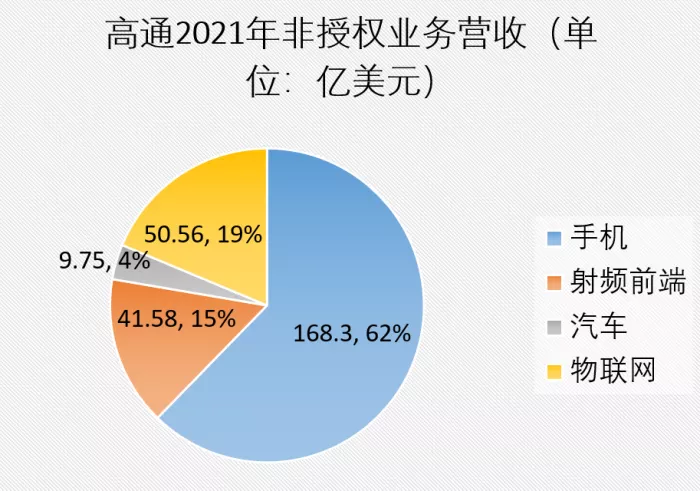

In 2021, Qualcomm continued to be the world's largest chip design company, with unlicensed business revenue of US $27 billion, mainly including smartphone products, RF products and Internet of things products.

According to the financial report of 2021, due to Apple And other OEM manufacturers increased demand for 5g products. Qualcomm's smartphone products increased by $6.369 billion, of which $3.6 billion was due to Qualcomm's SOC shipments.

In addition, Qualcomm's revenue from RF products increased by $1.796 billion, automotive products increased by $331 million, and IOT products increased by $2.03 billion.

▲ revenue of Qualcomm's businesses in 2021 (data source: Qualcomm's 2021 financial report)

2. NVIDIA: bet on artificial intelligence to become the leader of AI computing

NVIDIA was founded in 1993. Its original intention is to develop an image rendering chip in PC. In 1995, NVIDIA launched its first product nv1, but the sales volume was poor.

After 1997, NVIDIA beat its original competitor 3dfx in the field of image rendering chips and established its market position through subsequent products such as NV3, TNT and tnt2. With the increasing demand for games and video, NVIDIA launched its first GPU (graphics processor) in 1999, which was widely praised.

In 2004, NVIDIA founder Huang Renxun found that GPU was far more efficient than CPU in parallel computing. Therefore, NVIDIA began to develop CUDA Programming Tools, which laid a solid foundation for GPU to become a general-purpose processor. In 2012, Geoffrey Hinton at the University of Toronto submitted a deep convolution neural network algorithm called alexnet, which won the first place in the Imagenet computer vision challenge. The algorithm was trained with NVIDIA GTX 580 GPU. The error rate is only 16%, and the error rate of the second place is more than 56%.

Due to the advantages of GPU in artificial intelligence algorithm and parallel computing, GPU has gradually become a general chip in the field of Artificial Intelligence Computing and data center. NVIDIA, which laid out artificial intelligence early, has become a big winner in the era of artificial intelligence.

NVIDIA's revenue in fiscal year 2022 reached US $26.91 billion, an increase of 61% year-on-year, mainly due to NVIDIA's game, data center and professional visualization business.

In fiscal year 2022, NVIDIA's game business increased by 61% year-on-year to US $12.46 billion; The revenue of the data center increased by US $10.6 billion year-on-year; The revenue of professional visualization business increased by 100% to US $2.11 billion; The automotive and robotics business grew 6% to $566 million.

Among these NVIDIA businesses, the three most important revenues of game business, data center and professional visualization all set new revenue records, helping NVIDIA surpass Broadcom to become the second largest chip design company.

▲ business revenue of NVIDIA in fiscal year 2022 (data source: financial report of NVIDIA in fiscal year 2021)

3. Broadcom: anhuagao has become a "new" Broadcom with a small swallow

Founded in 1991, Broadcom is an industry leader in the field of communication. In 2000, Broadcom launched a crazy acquisition and made more than five acquisitions in the communication field, with a total amount of more than 6 billion euros.

Since then, Broadcom has completed M & A transactions in multimedia and storage businesses, including the acquisition of silicon spic for 1.4 billion euros and netlogic microsystems for 2.8 billion euros.

However, "acquisition madman" Broadcom has also been acquired one day. After acquiring LSI, an American chip supplier, for us $6.6 billion, anwago acquired Broadcom for us $37 billion in 2015, completing the famous "small swallow big" in the semiconductor industry. Since then, the new Broadcom has continued to maintain its leading position in the fields of communication, multimedia and so on.

In November 2017, Broadcom also made a takeover offer to Qualcomm, proposing to acquire all the outstanding shares of Qualcomm at an amount of US $105 billion, and then raised the offer to US $121 billion. However, in March 2018, US regulators rejected Broadcom's plan to acquire Qualcomm on the grounds of national security issues, and this amazing acquisition ended in failure.

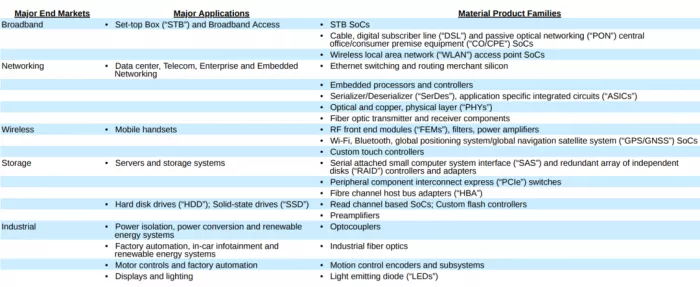

In 2021, Broadcom's revenue was US $27.45 billion. Its main products include set-top box SOC, wired network chip, RF front-end module, Wi Fi chip and other semiconductor products and software services.

▲ Broadcom products and terminal market (picture source: fourth quarter financial report of Broadcom in 2021)

4. MediaTek: starting with DVD chip, it has become the first smartphone SOC shipment

MediaTek was founded by caimingjie from Taiwan, China. He was the first person in Taiwan, China to introduce semiconductor technology, nicknamed "the godfather of Taiwan IC Design". In 1997, MediaTek was founded in Hsinchu Science Park, Taiwan, China.

MediaTek first started by relying on optical disc storage technology and DVD chip, integrating the originally expensive video and digital decoding chips, and providing software solutions, which greatly reduced the price of DVD. In 2001, MediaTek accounted for 60% of the DVD chip market and was listed on the Taiwan Stock Exchange in the same year.

In 2003, MediaTek entered the mobile phone chip industry, and also through high integration, it can provide mobile phone chips and software solutions at low cost. Its solutions are adopted by many fake mobile phones, and the industry is known as the "father of fake mobile phones".

In the era of smart phones, MediaTek's cost-effective strategy has been selected by Huawei, ZTE and other domestic mobile phone brands to enter the medium and low-end smart phone market and become the main competitor of Qualcomm.

In 2021, MediaTek's revenue was NT $493.415 billion (about RMB 112.795 billion), an increase of 53.2%, hitting a record high for two consecutive years, and its net profit was NT $231.605 billion (about RMB 52.945 billion), a year-on-year increase of 63.6%.

According to Cai Lixing, CEO of MediaTek, its products have been applied to 2 billion electronic devices, and all businesses have achieved growth. In terms of smartphone business, MediaTek's main revenue growth comes from the growth of 5g smartphone sales, and it is expected that its 5g shipments outside China will double in 2022.

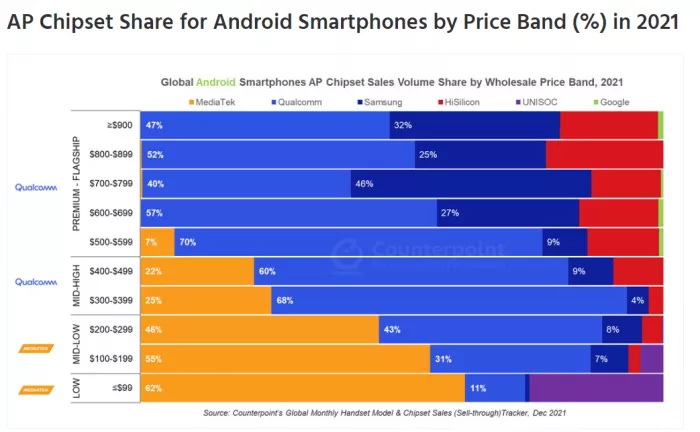

According to the data of market consulting firm counterpoint, MediaTek's shipments accounted for 46% of Android smartphone SOC and 35% of Qualcomm's in 2021. Most of the market share growth of MediaTek comes from the medium and low-end market where the mobile phone price is less than $299, while Qualcomm occupies a dominant position in the SOC and RF front-end of medium and high-end models above $399.

▲ share of Android mobile phone AP / SOC chipset by price in 2021 (picture source: Counterpoint)

5. AMD: after 50 years of entanglement with Intel, Su Ma led her to rejuvenate her vitality

Amd was founded in 1969. Its founder Jerry sanders and Intel founders are also from Fairchild Semiconductor. They are just sales executives, not technology bosses. In Sanders' own words: "Intel pulled $5 million in venture capital in five minutes, while amd took 5 million minutes to pull $50000."

Due to the affection of colleagues, Intel co-founder Robert Noyce financed AMD and authorized AMD to sell Intel processors. Therefore, AMD, as a "second supplier", focuses on cost performance and occupies the high-end and low-end markets respectively with Intel.

In 1981, Intel's groundbreaking 16 bit 8086 processor received an order from IBM. It is reported that due to limited production capacity, IBM asked Intel to authorize AMD to jointly produce.

However, the time of cooperation between the two companies was not long, and Intel and AMD had great differences in licensing. The two sides had a long lawsuit from 1987 to 1994. Finally, amd won the lawsuit and obtained x86 authorization.

Although amd won the lawsuit, in 1993, Intel launched the 586 (Pentium) with a sharp rise in performance, leaving amd behind. After that, amd began to launch self-developed processors and began to compete with Intel at the technical level.

During this period, AMD and Intel's products have won or lost each other and become a pair of "sworn enemies". At the Intel IDF developer conference in March 2005, amd even funded the flight performance team to pull out the words amd "turion 64" over it.

▲ amd flight show team writes "turion 64" in the air

In 2006, amd acquired ATI, the second largest GPU player at that time, for $5.4 billion, spanning both CPU and GPU markets. However, less than two years later, amd sold the imageon product line of ATI's mobile business department to Qualcomm for $65 million, missed the mobile market and gradually fell into a disadvantage. When it was at its worst, amd even considered selling the company's headquarters building.

In 2014, Su Zifeng took over as the CEO of AMD. By building better products, strengthening customer cooperation and simplifying business processes, Su Zifeng focused on the markets such as games, data centers and embedded devices, and regained vitality.

In October 2020, amd launched the acquisition of Xilinx, the leader of FPGA in the United States, with a transaction amount of US $35 billion. In February 2022, amd announced the formal completion of the acquisition of Xilinx with the consent of national regulatory authorities.

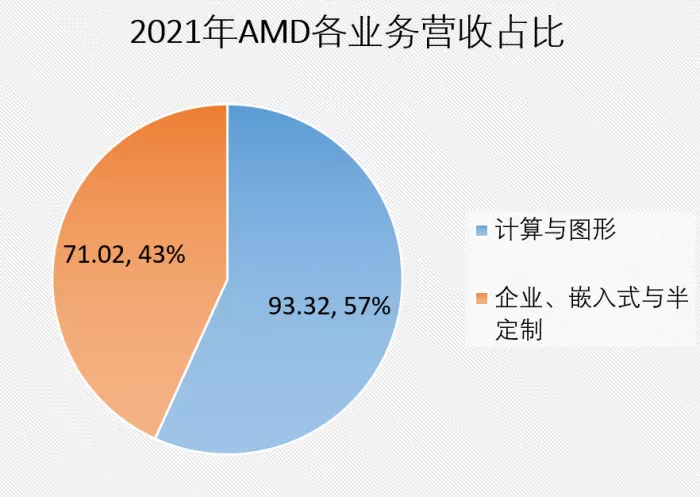

In 2021, AMD's revenue was $16.4 billion, an increase of 68%, mainly due to the growth of the revenue of computing and graphics and enterprise, embedded and semi custom.

The revenue of its computing and graphics department was US $9.332 billion, with a growth rate of 45%; The revenue of embedded and semi customized parts was US $7.102 billion, an increase of 113%.

▲ proportion of AMD's business revenue in 2021 (picture source: AMD financial report in 2021)

04. Conclusion: Moore's law promotes oligopoly, and a new node in the chip design industry is coming?

In the past two years, due to the impact of COVID-19, the demand for chips in smart phones, data centers, PCs and other fields has increased rapidly, and the revenue of chip design giants such as Qualcomm, NVIDIA, Broadcom, MediaTek, amd has also shown a rapid growth trend. In order to ensure their own technical strength and product competitiveness, these chip design giants are opening up new product lines: Qualcomm began to strengthen its automotive and AR / VR businesses; NVIDIA promotes the data center strategy of GPU + CPU + DPU and also acquires arm; Amd acquired Xilinx and strengthened FPGA.

For the chip design industry, on the one hand, emerging technologies such as 5g, artificial intelligence and big data are developing rapidly, and the requirements of chip performance and power consumption continue to improve. On the other hand, Moore's law is facing a bottleneck, and the chip design cost of advanced processes is increasing. Therefore, only a large enough chip market can accommodate advanced process chips, and only industry leaders have the power and ability to carry out product iteration, which promotes the fault between oligopoly market and chip design companies.

In the future, as countries strengthen their awareness of ensuring their own semiconductor supply, they will be more alert to the mergers and acquisitions of semiconductor giants. In the post Moore era and post epidemic era, the chip design industry with oligopoly competition may enter a new node.