Vietnam has become the focus of attention. Judging from many reports on the Internet, Vietnam is now thriving We were amazed that Vietnam's exports exceeded Shenzhen, Li Ka Shing switched to Vietnam after withdrawing capital from the UK, Nike ADI Samsung factory moved to Vietnam, and some even worried that Vietnam would replace China as a new "world factory"

With the rise of China's labor cost, Vietnam has attracted the transfer of labor-intensive industries such as Nike, ADI and UNIQLO with the advantage of cheap labor. In addition, Europe and the United States have low tariffs on Vietnam and Vietnam's local preferential tax policies, which have attracted many foreign investors to invest and build factories.

*With the advantages of demographic dividend, tariff and tax preference *, Vietnam's economy has indeed developed rapidly in recent years. According to the world economic outlook, Vietnam ranks 14th with an average economic growth rate of 5.99% from 2010 to 2021. Although it is not comparable to China's 7.24%, this growth rate has left many countries behind.

Vietnam's rapid economic development, stock prices and house prices also soared Over the past 10 years, the Ho Chi Minh index has soared from around 400 to around 1340, more than tripling. In particular, Vietnam's epidemic situation improved in 2020. After the liberalization of epidemic prevention measures, Vietnam's stock market ushered in a wave of severe blows, outperforming the global market index by 90%.

Not only the stock market, but also house prices in Vietnam. In April this year, the average price per square meter of real estate commercial housing in Ho Chi Minh City, Vietnam's economic center, reached a staggering US $3300 (about 21800 yuan), a year-on-year increase of 27%, a new high in recent ten years; The average price of houses in the capital Hanoi also rose by more than 20% year-on-year.

The fast-growing economy, soaring stock prices and house prices show the prosperous side of Vietnam, but this is not the whole truth

Li Ka Shing's investment in Vietnam may be a focus on the real estate development opportunities in the process of urbanization in Vietnam. At the beginning, Li Ka Shing entered with abundant capital during the rapid development of real estate in mainland China around 2010. A few years later, he had a hunch that there might be a bottleneck in mainland real estate, so he cashed out and left.

In order to stimulate the economy hit hard by the epidemic, in January this year, Vietnam adopted an economic stimulus policy of up to 350 trillion Vietnamese Dong (about US $15.21 billion), nearly one-third of which was used to invest in infrastructure and wanted to take the road of infrastructure driven urbanization. There is a feeling of copying China's "4 trillion" economic stimulus in 2008.

From the perspective of historical experience, it is often the capital that leaves after earning a full pot, leaving the fried high house prices to the local people to bear. The current housing price income ratio in Ho Chi Minh City is enough to make ordinary citizens despair, let alone in the future.

In addition, although Vietnam's exports exceeded that of Shenzhen in the first quarter of this year, Shenzhen's trade surplus was more than seven times that of Vietnam. In the first quarter of this year, Vietnam's exports of goods amounted to US $89.1 billion. After deducting the imports of US $87.64 billion in the same period, the trade surplus was only US $1.46 billion (about 9.73 billion yuan). Over the same period, Shenzhen's exports amounted to 407.66 billion yuan, its imports 332.82 billion yuan, and its trade surplus was 74.84 billion yuan.

*From the GDP data, Vietnam is not only far behind Shenzhen, but also behind Guangxi *. In 2021, Vietnam's GDP was 362.6 billion US dollars (about 2400 billion yuan), and its per capita GDP was about 3700 US dollars (about 24000 yuan); Shenzhen's GDP is 3066.4 billion yuan; Guangxi Province is 2474 billion yuan, with a per capita GDP of 49000 yuan. It can be seen that the GDP of Guangxi Province was higher than that of Vietnam last year, and the per capita GDP was more than twice that of Vietnam.

From the above data, it is not difficult to see that Vietnam is not as good as many people think, and Shenzhen is not as bad as they think.

What's more, Vietnam is a country with a population of nearly 100 million, while Shenzhen is only a Chinese sub provincial city with a population of more than 17 million, which is really incomparable.

The rapid development of Vietnam's manufacturing industry in recent years is not because of its strong technology and competitiveness, but because just caught up with the tuyere of industrial transfer and happened to have the advantage of low cost, which attracted the transfer of labor-intensive industries**

01 beneficiaries of industrial transfer

In recent decades, the global industrial chain has undergone several major shifts.

Around 1960, the United States, Japan, Germany and other developed countries gradually transferred labor-intensive industries to South Korea, Singapore, Taiwan, China and Hong Kong in order to reduce production costs after their domestic industries were saturated. After these places undertook the industrial transfer, the industrialization process continued to accelerate and their economies developed rapidly, becoming the "four little dragons of Asia".

With the industrial upgrading of the "four little dragons of Asia", after 1980, labor-intensive and high energy consuming industries were successively transferred to Thailand, the Philippines, Malaysia, Indonesia, China's coastal areas and other places. With the rise of China's labor costs and the acceleration of industrial upgrading, some manufacturing industries with low added value have gradually shifted to Vietnam.

Vietnam's industry can develop by industrial transfer and foreign investment. Since 2015, more than 70% of Vietnam's exports have been contributed by foreign-funded enterprises, and the export growth rate of foreign-funded enterprises in Vietnam is much higher than that of local enterprises.

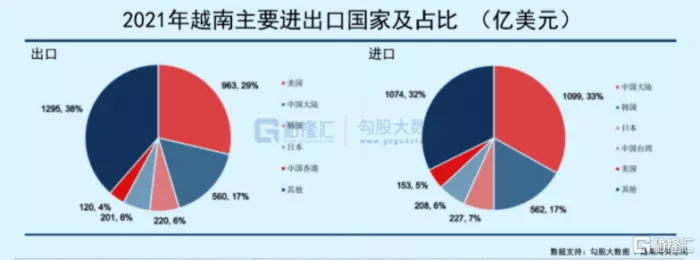

From the perspective of import and export structure, Vietnam mainly imports raw materials, parts and production equipment from China, South Korea and other countries, and then exports the products to the United States, the European Union and other places .

33% of Vietnam's total imports come from Chinese Mainland, mainly textiles, leather materials, mechanical equipment, telephones, mobile phones and parts. In addition to Chinese Mainland, Vietnam also imports products from South Korea, Japan, Taiwan, China, the United States and other places.

Vietnam's largest buyer is the United States, accounting for about 29% of the total exports. Among the products exported to the United States, timber and products, textiles and clothing, machinery and equipment account for more than 40%. In addition to the United States, China, South Korea and Japan are also the main export targets of Vietnam.

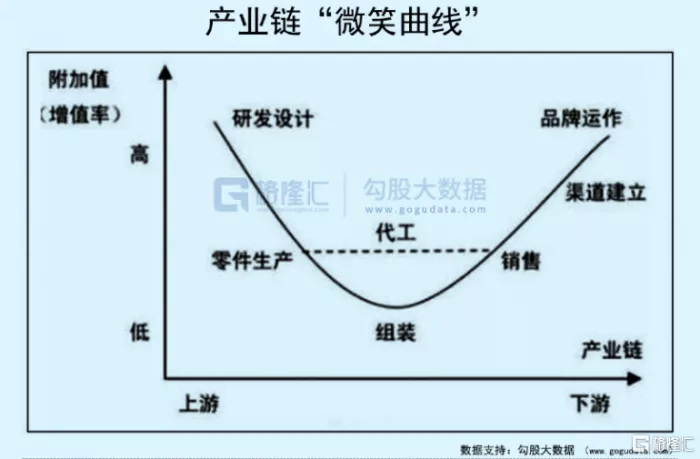

Vietnam's current industrial development model is similar to that of the processing plants with supplied materials in China's coastal areas 30 years ago. Relying on cheap labor to earn the money assembled in the "smile curve" of the industrial chain, the profit space is very small, while the money in R & D, design, brand, sales and other links with large profit space can not be matched, because Vietnam has neither technology nor market, but only cheap labor**

**Demographic dividend is the key to attracting the transfer of labor-intensive industries. Vietnam has a population of nearly 100 million. In 2017, the median age of Vietnam's population was only 30.5 years old, and the average wage was only one third of that of China. The large number of young people and low average income are important advantages for Vietnam to develop processing and manufacturing industry.

In order to attract investment, Vietnam has given many preferential policies to enterprises. The draft submitted by the Vietnamese Ministry of Finance in 2016 shows that in 2017-2020, the enterprise income tax rate will be reduced from the previous 20% to 17%, and enterprises with an annual turnover of no more than vnd 100 billion can enjoy tax exemption. In addition, the low tariffs given to Vietnam by European and American countries have further reduced the export cost of enterprises.

Lower labor and rental costs, combined with preferential tariffs and taxes, have enabled Vietnam to undertake the transfer of some labor-intensive industries in China's coastal areas, and the manufacturing industry has developed rapidly.

02 how far is it from the "world factory"?

The industrial transfer undertaken by Vietnam has indeed replaced some of China's export products, but it is basically products with low technical content such as furniture and tires.

According to panjiva, a trade data company, furniture imports from retailers such as home depot and IKEA decreased by 13.5% from China and increased by 37.2% from Vietnam; In terms of automobile tire imports, the United States' imports from China decreased by 28.6%, and its imports from Vietnam soared by 141.7%.

What is really affected by Vietnam are those inland provinces that want to undertake the transfer of coastal low-end manufacturing, because many processing and manufacturing industries have not been transferred to inland provinces, but to Vietnam In the first quarter of this year, Vietnam's total foreign investment was US $10.8 billion, a year-on-year increase of 86.2%, half of which came from China.

But this does not shake China's position as a "world factory", because China's manufacturing competitiveness has risen to the second in the world, second only to Germany** In April 2021, according to the data of the United Nations Industrial Development Organization, China's manufacturing competitiveness has risen from the fifth in the world in 2012 to the second. With an industrial GDP of nearly $4 trillion, China is the country with the largest manufacturing industry. The output of cars, mobile phones, computers, washing machines, air conditioners, color televisions, refrigerators, steel and other products ranks first in the world.

The industries undertaken by Vietnam are basically labor-intensive industries with little technical content. Although it has a certain impact on inland provinces that want to undertake the transfer of coastal low-end manufacturing, Vietnam has neither high-end manufacturing nor heavy industry, nor can it establish a full industry chain network like China. For China that wants industrial upgrading, Vietnam is more industrial complementarity.

Moreover, Vietnam's demographic and tax advantages cannot be sustained. With more and more foreign investors investing in Vietnam, the cost of local labor and rent is increasing rapidly. A survey shows that the average monthly salary of factory employees in Vietnam this year is 2200 yuan to 2400 yuan. Enterprises generally expect that the labor cost in Vietnam will be the same as that in China in seven years. In terms of rent, the rent of industrial parks in the provinces around Ho Chi Minh City has increased from $30 per mu in 2015 to $100 today, which has doubled several times.

European and American tariff preferences for Vietnam are also facing the risk of being cancelled. After all, the decision is in the hands of others. As early as 2020, the United States launched a 301 investigation on Vietnam's timber and exchange rate related policies. It can be seen that it takes minutes to impose tariff sanctions on Vietnam.

The current situation is that Vietnam's population and rental costs are rising. Once the tariff advantage is lost, Vietnam's manufacturing industry will face great challenges.

03 next Thailand?

Although Vietnam cannot replace China as a new "world factory", it is hopeful to become the next Thailand.

As a neighbor of China, Vietnam followed the pace of China and issued the investment law in 2006, which abolished many previous restrictions on foreign investors. Then it joined the WTO and officially integrated into the global trading system. Its foreign trade developed rapidly and its economy grew rapidly.

In the 20 years from 2000 to 2020, Vietnam's GDP has more than doubled. Per capita GDP also soared from $96 in 1990 to around $3700 last year.

According to Ruan Chunfu's goal, Vietnam will become a high-income country by 2030, with a per capita income of US $18000; By 2045, China will become a prosperous and stable developed country.

This goal is not grand, but in just a few decades, it is more difficult for Vietnam to become a developed country like Japan and South Korea. But with luck, it is still possible to reach the level of Thailand , and some Vietnamese economists regard Thailand as their development goal.

Vietnam and Thailand are both major rice exporters in the world, and there are many tropical fruits. We can continue to follow the route of earning foreign exchange through agricultural products export. In terms of tertiary industry, Vietnam has a long and narrow coastline and good winter tourism resources, so it can develop tourism like Thailand.

In terms of industry, Vietnam is dominated by labor-intensive light industry, which is seriously homogenized with Thailand and other Southeast Asian countries. When the labor cost rises to the level of Thailand, it has no advantage compared with other Southeast Asian countries, so it is very difficult to continue to move forward.

In the long run, Vietnam can learn from South Korea and Japan, select several leading industries in the fields of textile, automobile and electronics, and establish corresponding industrial chains and supporting networks.

However, this requires long-term accumulation, and in the increasingly fierce global competitive environment, Vietnam, the latecomer, has many difficulties to succeed.

In addition, in the process of borrowing heavily to develop the economy, it is very dangerous to encounter the global liquidity crunch caused by the Fed's interest rate hike** Thailand is a living example. Thailand, which successfully captured the second wave of industrial transfer in those years, was ruthlessly harvested in the 1997 Asian financial crisis triggered by the US Federal Reserve's interest rate hike as soon as its economic development improved. Now the sickle of the Fed's interest rate hike has been held high, and it is still a question whether Vietnam, with a weak family background, can bear it.

The IMF and some big Wall Street banks believe that the risk of the Fed's tightening policy is being passed on to vulnerable and poor countries by using the tightening dollar cycle. under the impact of the surge in external debt and the inversion of foreign exchange reserves, vulnerable countries such as Turkey, Sri Lanka, Vietnam, Brazil and Argentina will face the dilemma of rising financing costs and increasing debt interest .

It is undeniable that Vietnam has made great efforts to develop its economy and its industrialization and exports have also improved over the years, but it is extremely difficult to complete the counter attack from a poor country to a rich country. There are many traps in the process. If Vietnam can get away with it, it is still possible to catch up with Thailand.